The State of L2: Q1-2024

Brief

Welcome to the latest edition of the State of L2 Report for Q1 2024. In this report, various metrics related to Layer-2 solutions are analyzed and presented to the reader. Also, a survey has been conducted to analyze the behavior of L2 users in the last quarter.

According to the results of the graphs and survey, an analysis of the direction of Layer-2 activity, as well as the gains and losses of projects, has been anticipated. The sources of the data include L2Beat, Growthepie, Defillama, and the official block explorers of the networks. Some graphs have utilized mixed data obtained from multiple sources.

L2 in Numbers

Total Value Locked

According to the L2Beat, the total value locked on L2 scaling solutions increased from $23 billion to $39 billion during the first quarter of 2024. This corresponds to a 69.57% increase in the first quarter of the year. The increase in terms of Ether amounted to approximately 10,072,000 Ether to 12,375,000 Ether, which translates to an approximate 18.61% increase.

During the first quarter of the year, the changes in TVL among the top 10 L2 chains occurred as depicted in the graph. The highest increase, at 86%, occurred in the Base network.

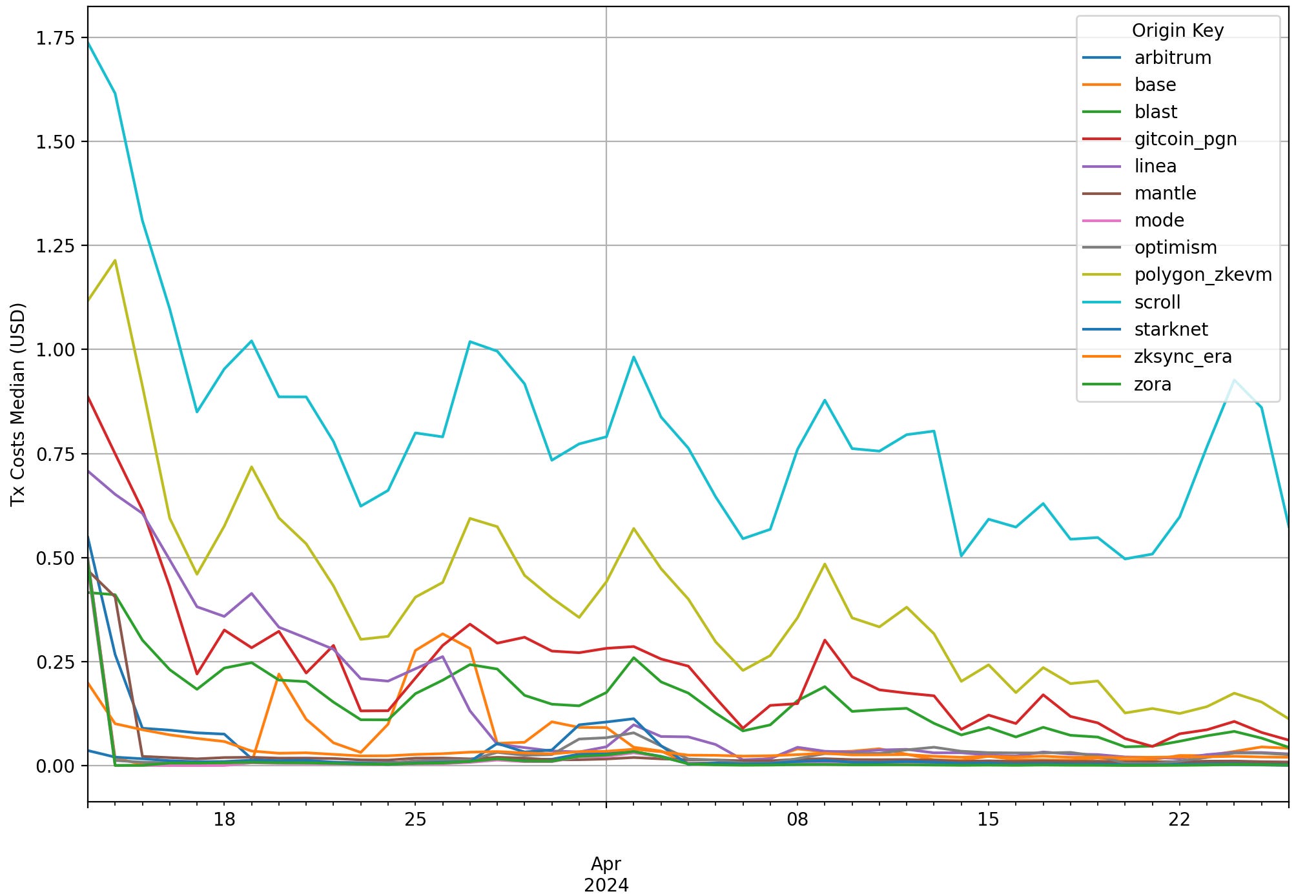

Post-Dencun Transaction Fees

The majority of costs for Ethereum rollups are generated by CALL DATA. The Dencun update aims to create a data area in blocks specific to rollups, called a blob, thus dramatically reducing rollup transaction fees. The chart shows the change in transaction fees for rollups with the Dencun update.

Protocol Count

When comparing the number of protocols on L2 networks, we can say that Arbitrum leads by more than twice as much as its closest competitor with 606 protocols. Following Arbitrum are Base, Optimism, and zkSync Era, respectively.

When examining the increase in the number of protocols on L2 networks, Arbitrum saw the highest increase with 162 new protocols, followed by Base, Optimism, Linea, and others, respectively.

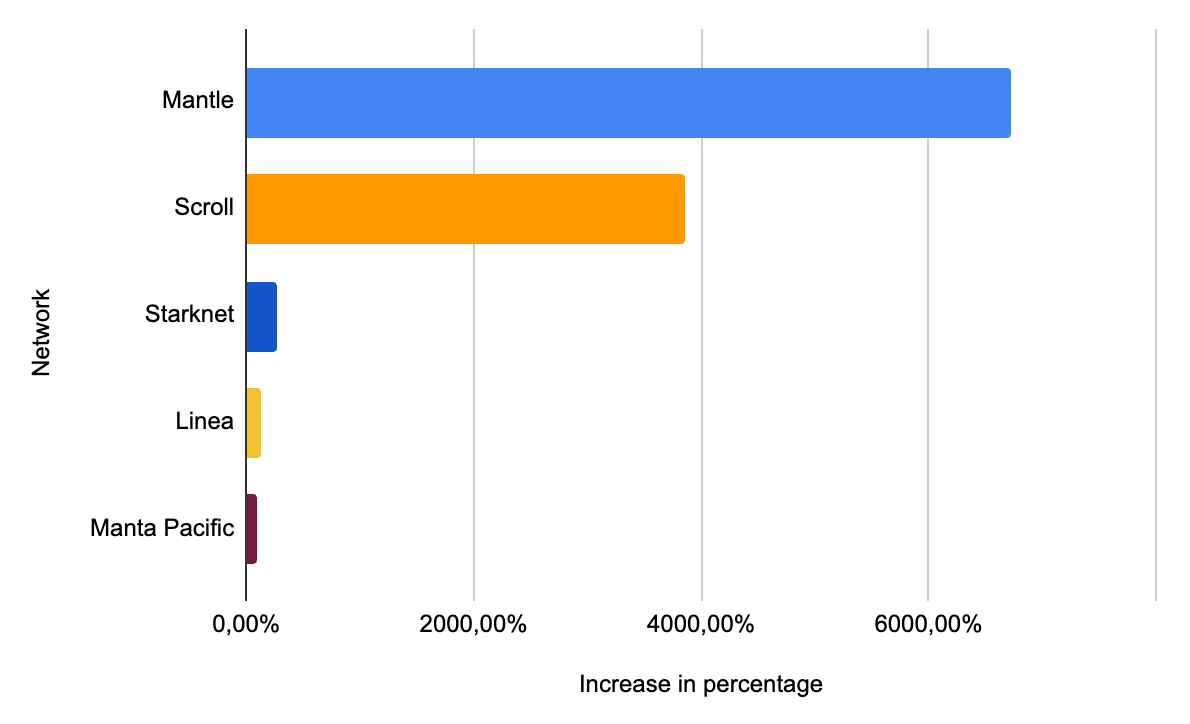

Unique Addresses

The above visual shows the top 5 L2 networks based on the increase in unique address count. Mantle leads with a 60x increase, followed by Scroll, Starknet, Linea, and Manta Pacific, respectively.

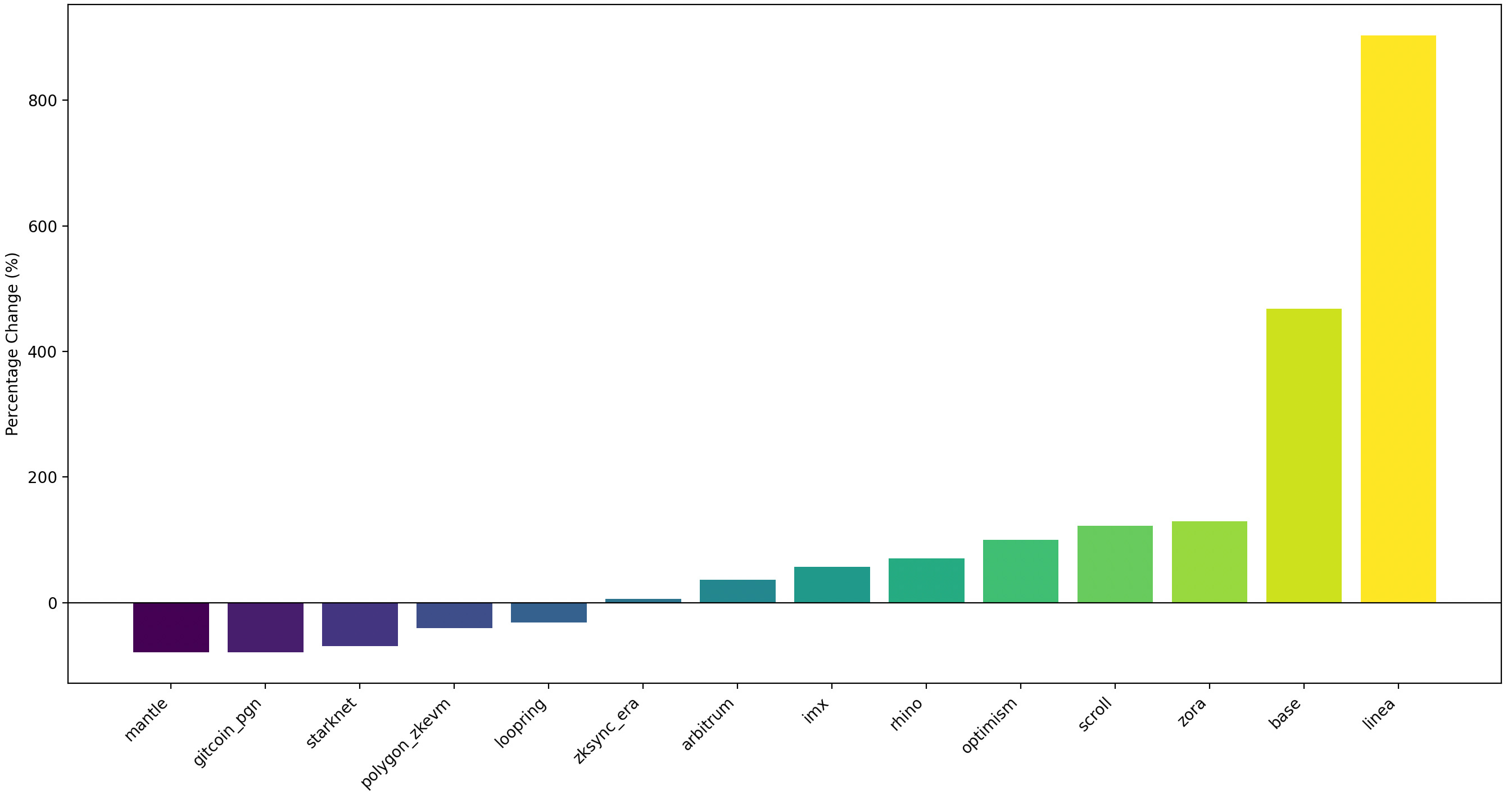

Daily Active Addresses

When we look at the daily active addresses count, Linea appears to have the highest number of active users by the end of the first quarter. Following Linea are zkSync, Base, Arbitrum, and Optimism, respectively.

When we look at the change in daily active addresses count between the first and last days of the first quarter of 2024, Linea maintains its leadership with an 8x increase. Following Linea are Base, Zora, Scroll, and Optimism, respectively.

Daily Transaction Count

The above graph displays the daily transaction counts on L2s. While zkSync maintained its leadership for much of this quarter, the daily transaction count on Linea significantly increased in the final days, allowing Linea to take the lead in daily tx counts.

At the beginning and end of the first quarter, when comparing the daily transaction counts, Linea emerged as the Layer 2 network with the greatest increase. Linea was followed by Base, zkSync, Optimism, and Scroll in that order.

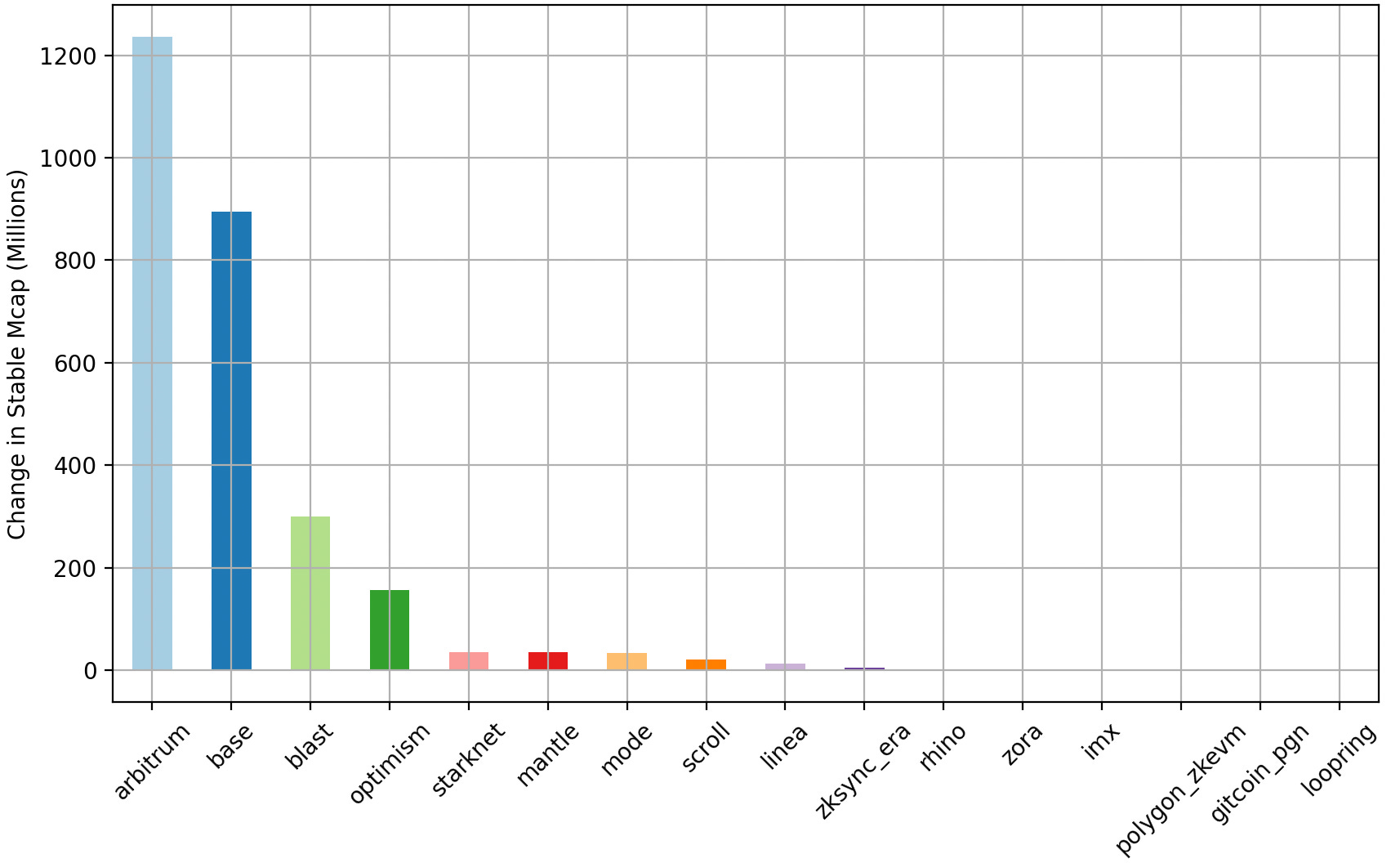

Stablecoin Marketcap

In this quarter, Arbitrum saw the largest increase in stablecoin, with a rise of $1.2 billion. It was followed by Base, Blast, and Optimism, respectively.

Rollup Revenue

At the beginning of the year, some rollups were not very profitable, but by the end of the quarter, they had increased their profitability, especially the Base network, which had days when it made nearly $2.5 million in profit.

User Behavior Analysis Over the Last 3 Months

In order to analyze the behaviors of L2 users in the first quarter of 2024, L2 Planet created a 10-question survey. The survey analyzed users' motivations for using L2, their changing habits, and their future expectations from the beginning of the year to the end of the first quarter. A total of 102 users completed the survey.

Of those surveyed, 58% identified themselves as members of the crypto community, 36% as crypto traders, and 6% as developers.

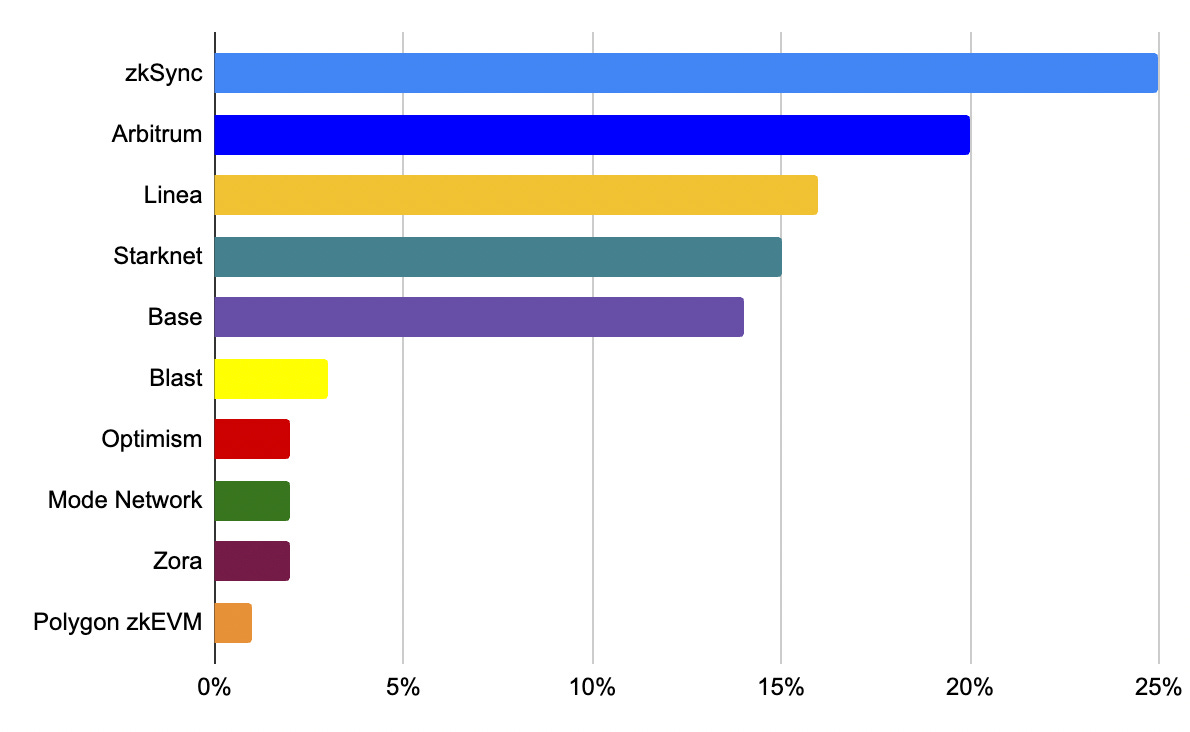

25% of users reported that they used zkSync Era the most over the past three months, followed by Arbitrum, Linea, Starknet, and Base, respectively.

In the first quarter, users found Starknet to be the least successful project. It seems likely that this result stemmed from Starknet losing a large user base due to the $STRK airdrop. Following Starknet, Polygon zkEVM, Manta Pacific, Scroll, and Linea are respectively ranked.

A large majority of users, nearly 70%, use L2 networks for airdrops. Only 27% of users utilize L2s because they are cheap, while 4% use them for their speed.

73% of users have seen an increase in their use of L2 following the Dencun update. This can be interpreted as a result of the reduced transaction fees on L2 networks.

77% of users believe that L2 networks have become sufficiently affordable following the Dencun update. This result clearly demonstrates the significance and impact of the Dencun update.

When examining users' favorite newly launched L2 network over the past three months, Blast, supported by Paradigm, leads the race. It is followed by Mode Network, Hyper, Astar zkEVM, and Karak, respectively.

Half of the users view the OP Stack as the most successful rollup stack in the last three months. Surprisingly, zkSync Hyperchains is seen as more successful than Arbitrum Orbit according to users.

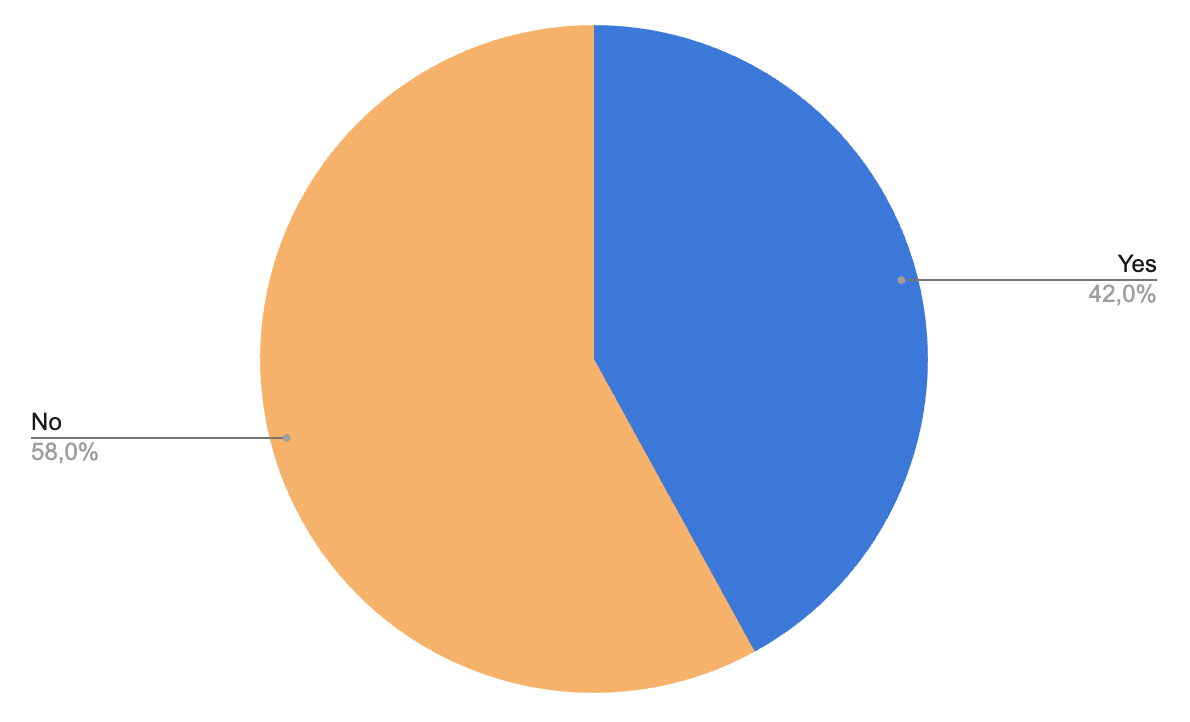

To measure the level of Layer-3 adoption, users were asked whether they had used any L3 networks in the last 3 months. 58% of users stated that they had not used any L3 networks during this period.

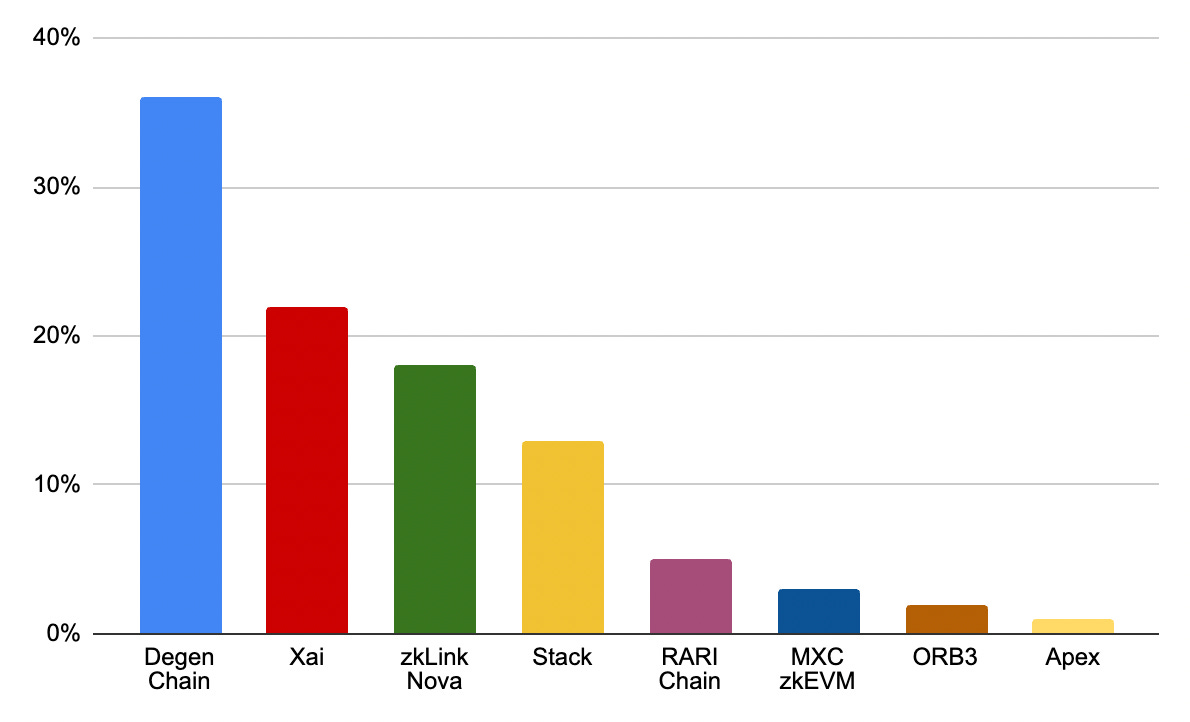

Users were asked which Layer-3 solution excites them the most. Degen Chain topped the list with 36%, followed by Xai, zkLink Nova, and Stack.

Conclusion

Considering both metric graphs and survey results, we see two prominent L2 solutions: Base and Linea.

We observe that organic activity on Base is reflected in the network's total value locked, number of protocols, transaction count, rollup revenues, and stablecoin growth. Linea leading in some metrics can be explained by the traffic generated by the LXP scoring system.

Looking at the user behavior survey, the importance of the Dencun update is evident once again. Post-Dencun, L2 solutions have become cheaper and attracted more users. zkSync being the most preferred network in the last three months could be interpreted as users increasing their activity for a potential airdrop. Indeed, the results clearly show that the main motivation for using L2 solutions is airdrops. Starknet, which conducted an airdrop criticized by many, turned out to be the least successful L2 solution in the last three months. We see once more the significance of the relationship between airdrops, the community, and L2.

Lastly, we see that the adoption of L3 networks has not fully materialized yet, and aside from a few standout projects, L3s have not reached a sufficient user base.